Virtual Banking Services for International Businesses

B2B Pay has been helping 3000 companies collect payments from all over the world, pay suppliers abroad and convert currency at lower costs than a traditional bank.

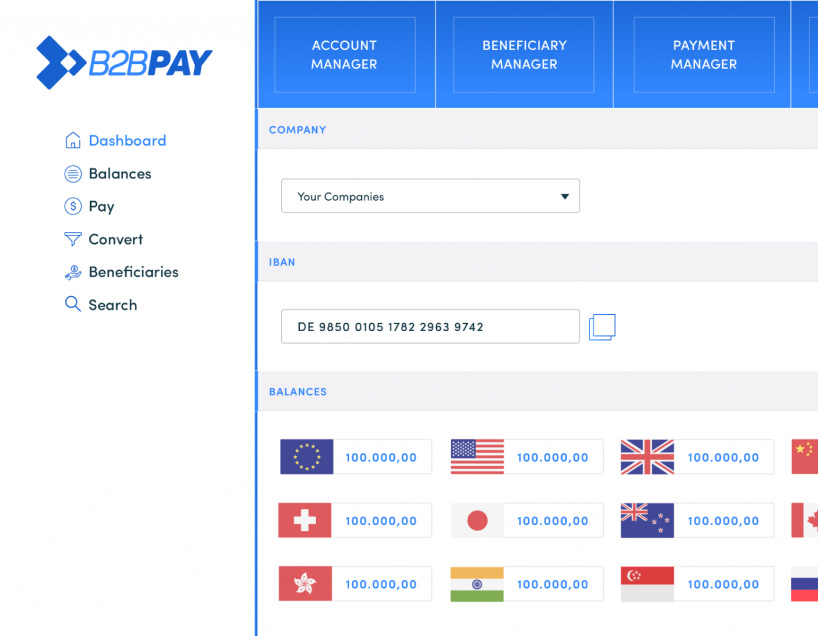

A Smart Online Bank Account to receive and store multiple currencies using one single European IBAN. Collect payments from customers, marketplaces and credit card processors, convert to 30+ currencies and transfer money internationally to 170+ countries. The user-friendly dashboard provides you full control of your transactions.

Accept 20+ cryptocurrencies and convert instantly to Euro at the best market price. Using our powerful dashboard you can choose to hold funds in different currencies and manage risk and volatility.

Accept online card payments (including MasterCard, VISA, Amex) from 170+ countries. Cards are processed via major acquiring banks such a Société Générale that guarantee funds up $100.000 per customer. Full dashboard access to manage transactions and API integration. Lower prices than major card processors like Stripe.

Just starting your business? A simple, no frills SEPA EUR IBAN account for sending and receiving faster payments. Receive payments in EUR, USD, GBP, HKD and CNY and send funds out via SWIFT to 212+ countries.

Perfect for small business with European customers

We have been very happy with the service provided by B2B pay - in fact, their great service is why we chose them.

Blue Mobile Ltd, England

The application process is very easy and can be done completely online. Our account management is also fully digital.

Too Mobiles,

B2B Pay allows me to receive payments from Amazon, which wasn’t possible before. They made it easy for me to open an international account - even as a non-resident!

Melina Lewis, Tankwa Sky Holdings Pty Ltd, South Africa

We can now do business more easily with EU clients as B2B pay’s account offering has allowed us to accept SEPA payments.

Getting a new business off the ground is not easy; we have been there and know your pain. With over 50% of B2B pay customers being recently registered businesses, we have plenty of experience setting up accounts for startups

Own Bank accounts to collect from:

We provide local bank accounts in your company’s name in the USA, Europe, Germany, and Great Britain to collect payments directly from customers, payment processors, marketplaces.

Benefits:

We love startups not because we are one but also we want to grow with you. We've prepared for you the banking resources to grow your business and expand globally.

Non-Residents

Companies

Offshore

Our accounts are tailored for non-residents and offshore businesses. We can open cross border accounts for companies from 170+ countries. Our onboarding processes are fully digital and do not require visits to our offices.

Own Bank accounts to collect from:

We provide local bank accounts in your company’s name in the USA, Europe, Germany, and Great Britain to collect payments directly from customers, payment processors, marketplaces.

Benefits:

Full digital onboarding and bank accounts that are approved and managed online

Fintech

Fintech

Most banks struggle to work with fintech companies due to complex payments regulations. We love fintech and can help remove these barriers to build your vision.

Own Bank accounts to collect from:

We provide local bank accounts in your company’s name in the USA, Europe, Germany, and Great Britain to collect payments directly from customers, payment processors, marketplaces.

Benefits:

We can provide you with a starter pack to test your business model and help with collecting payments, currency conversions and APIs.

IT & Consulting

Drop Shippers

Modern IT and consulting firms need global bank accounts to receive international payments. Our customers are often global players with staff and suppliers located globally.

Own Bank accounts to collect from:

We provide local bank accounts in your company’s name in the USA, Europe, Germany, and Great Britain to collect payments directly from customers, payment processors, marketplaces.

Benefits:

We understand risk and are able to onboard IT and consulting business fast and pay consultants globally in 25+ currencies. We can provide local bank accounts in Europe and America.

E-commerce

E-shops

Drop Shippers

High Frequency

We can provide local business bank accounts within the USA and Europe to allow you to collect payments directly from customers, payment processors and marketplaces. Use currencies to unlock new customer segments, price more competitively and increase your margins.

Own Bank accounts to collect from:

Marketplaces: Amazon DE, Amazon US, Directly from customers, B2B, C2B, B2C

Benefits:

Banking for all online businesses, no high fees on currency change, track your payments easily through our dashboard.

Blockchain

Payment

Marketplaces

With our payments infrastructure, crypto exchanges can safely send and store fiat funds with reputed banks.

Own Bank accounts to collect from:

We provide local bank accounts in your company’s name in the USA, Europe, Germany, and Great Britain to collect payments directly from customers, payment processors, marketplaces.

Benefits:

We help exchanges manage their Fiat with funds held at reputed banks. Many of our customers use our accounts to buy and sell on P2P networks. We love blockchain projects and are happy to provide your project with an account for managing your operations

Why Trust Us

We are real people trying to solve real problems. To date, we have helped thousands of companies worldwide open up virtual bank accounts. The founding team has broad and in-depth experience in both finance and technology across government and global corporations. B2B is partnered with prestigious financial institutions. We started our journey when we took part in the Nordea Bank Accelerator Program in Helsinki, Finland and the Barclays Bank Accelerator program. Check out the winning Barclays pitch below:

We are doing our best to cater to the banking needs of entrepreneurs all over the world. Wheter you're a digital nomad in need of a virtual bank account, or you are a company looking to operate with SEPA countries in a quick and easy way, you need a bank to back you up. We got your back. We provide virtual banking services for international companies like yours.

Open your virtual account online and start banking.

Now, non-resident companies can get an IBAN within the EU. Powered by Barclays.

Problem:

Your company loses up to 20% off your margin on currency conversion and fees when you receive money from abroad. It’s time to stop losing money when getting paid.

Without B2B Pay, your company:

Cannot open a non-resident bank account in Europe

Cannot collect or send domestic wire transfers

Pays SWIFT fee of €30

Pays currency conversion cost of 3-6%

Cannot access EU payment gateways

Suffers from banking process bureaucracy

Cannot collect payments from marketplaces like Amazon

Waits 2-5 days per transfer

Solution:

Get a B2B Pay virtual bank account with a unique IBAN. Your new non-resident bank account is linked to your business bank account in your home country. You get a faster, 80% cheaper and transparent B2B transfer.

With B2B Pay, your company:

Gets its own non-resident bank account in Europe

Can receive free payments from 35 EU countries in 2-12 hours

Can make SEPA payments to 35 EU countries

Saves €30 SWIFT fee and +80% on Foreign Exchange (FX)

Can take advantage of FX conversion automation

Can integrate with marketplaces and payment gateways

Can make global payments in 138 currencies

Gets Instant notifications of incoming payments

Can take advantage of online onboarding

Not Resident Bank Account

A virtual bank account is suitable for anyone doing business abroad.

You can now receive the fastest B2B transfers from anywhere. Our Tier 1 partners give you access to any currency. We replace countless processes with a seamless conversion routine. Automation means you can send money to over 130 countries from any country with little to no effort. Our focus is on saving you money.

B2B payments should be free from bureaucracy. When you have a virtual bank account, B2B transfers are easier, faster and cheaper. You can monitor transactions in real-time. We use existing banking infrastructure to solve serious problems like reconciliation, cash management and pooling accounts.

The world of banking is changing fast. Fintech offers financial solutions using technology, creating a new layer on top of the old banking systems. Better integration, quicker processes and lower costs means you benefit, as these effects grow exponentially. We use the latest technology, so when you use B2B Pay you save money.

Virtual Banking API

We develop seamless, secure and economical banking products regardless of the market segment. From managing 250 million euros split in thousands of international transactions to the creation of a system with 10 thousand IBANs that handles factoring, we are ready.

Simple white-label solutions to complex problems. Our technological expertise provides you with the best in cutting-edge financial packages — designed with your business in mind.